Volatility: A Feature, Not A Bug

All LettersI hope your spring has been less chaotic than the headlines. They say March comes in like a lion and out like a lamb, but as we move into April, this year has felt like a Jackson Pollock splatter painting of economic and geopolitical news that hasn't quite settled into "lamb" territory yet. Between a tenuous cease-fire in the Middle East and a literal science-fiction report wiping out a trillion dollars in market value, it’s been a season that tests even the most disciplined investor. As we look at the first 90 days of the year, it’s helpful to step back and put some of the noise into context.

A Recap on the Year To Date

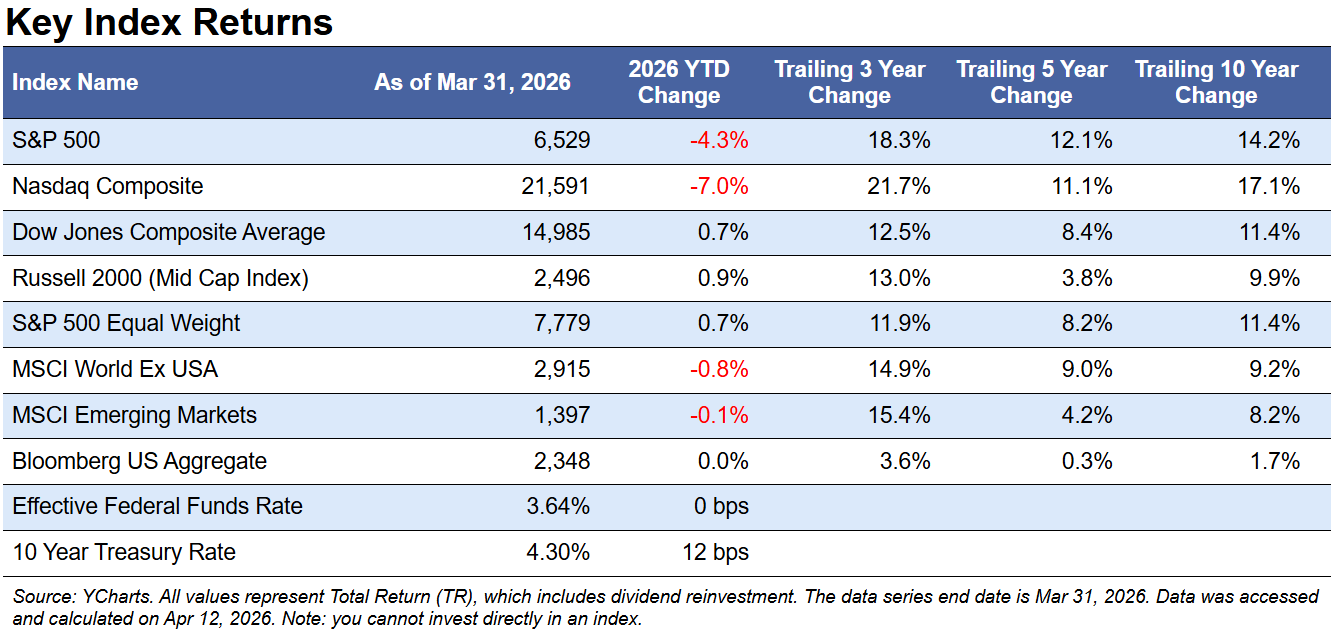

If you feel like the market has been a roller coaster, the data backs you up. As of March 31, 2026, the S&P 500 is down 4.3% for the year, while the tech-heavy Nasdaq has retreated 7.0% (and was down over 12% from the peak at one point in the quarter). We are currently marking the first anniversary of the "Tariff Typhoon," a period in early 2025 where the market fell nearly 20% in a matter of weeks before soaring to new highs.

We often tell clients to expect at least 10% drop once every year (called a “correction”), and 20% of their capital to "appear to disappear" temporarily every five years or so (called a “bear market”).

The phrase "it's not a bug, it's a feature" is a classic bit of tech industry tongue-in-cheek used to describe a situation where a piece of software behaves in an unexpected or broken way when it actually provides a hidden benefit or was intentionally designed that way for a specific reason. Essentially, it's the art of recontextualizing a quirk as an intentional functionality,

The same can be said for financial markets: volatility isn't a bug, it’s a feature. Volatility is the price of admission for the superior long-term return that equities have historically provided. It’s called the equity risk premium: equities have risk, which is expressed as volatility and experienced by the human brain as discomfort, for which investors are paid a premium over less volatile asset classes.

Oil: Classically Inelastic

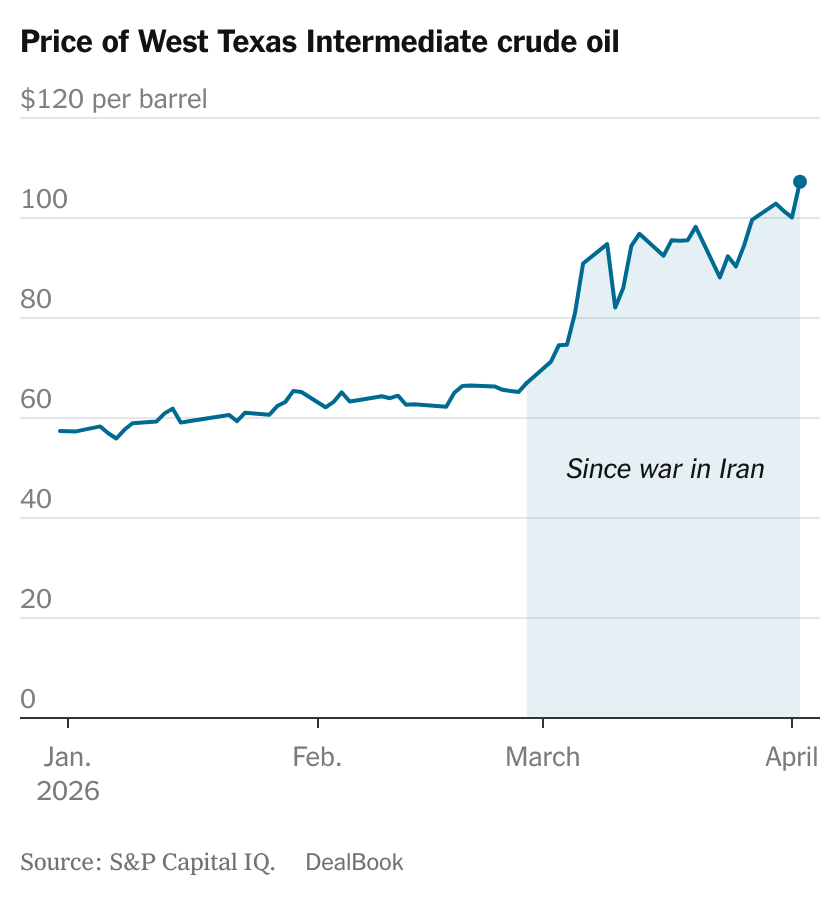

The recent surge in gas prices is a perfect lesson in the economic concept of inelasticity. Even though the Strait of Hormuz typically handles about 20% to 25% of the world’s energy shipments, the price of crude oil has jumped by nearly 50% since the conflict in Iran began. This happens because oil is a necessity, not a luxury. When the supply of oil is constricted (in this case due to conflict and shipping standing still), the whole world enters a desperate bidding war for the oil that is still available. Because most people cannot simply stop driving to work or heating their homes, they are willing to pay a much higher premium to get the fuel they need. This is why the spot price of oil (the current price for immediate delivery) skyrocketed well over $100 a barrel. In short, because oil is a must-have item with no easy substitute, a small drop in supply causes a significant spike in price.

Second Order Impacts: Fertilizer and Helium

The war in Iran has done more than just raise the price of a barrel of oil or a gallon of gas. We are seeing significant second-order impacts, particularly in agriculture. Disruptions in the natural gas market have sent fertilizer prices soaring, which economists expect will soon trickle down into higher grocery bills for everyday staples.

Far from being just for birthday parties, helium is a non-substitutable component in modern manufacturing. Its unique cooling properties are essential for semiconductor manufacturing (crucial for etching silicon wafers), data centers (high-capacity hard drives are helium-sealed to reduce friction), and healthcare (MRI scanners require liquid helium to keep magnets functional).

Qatar produces roughly one-third of the global supply of helium. Getting it to market requires transit through the Strait of Hormuz. With that route currently restricted and regional infrastructure damaged, we are seeing a significant supply shock.

AI Watch

The rate of change in artificial intelligence continues to accelerate. While daily headlines are difficult to keep up with, two events this quarter stood out for their potential long-term impact.

In February, Citrini Research released a widely discussed memo titled “The 2028 Global Intelligence Crisis.” Written as a fictional retrospective from the near future, the piece explores a world in which AI agents are increasingly replacing humans as opposed to simply augmenting human work. One concept that drew particular attention was “Ghost GDP” - an economic scenario where companies become dramatically more efficient through AI, yet overall demand weakens as displaced workers reduce spending. As the memo notes, machines don’t buy lattes or pay mortgages. Generally speaking, productivity improvements are thought to be one of the key drivers of economic growth. While entirely speculative, the memo highlights a real tension: AI productivity gains may not automatically translate into broad economic growth. The memo sparked significant debate across both technology and investment communities.

The second major development was the release of “Claude Cowork,” a new set of capabilities from Anthropic that demonstrated AI’s ability to execute complex software tasks with increasing autonomy (as if providing more support for the Citrini memo). Markets reacted quickly. Investors began reassessing the durability of traditional software business models, particularly those reliant on high per-seat subscription pricing. While talk of a “SaaS-pocalypse” may be overstated, the repricing across parts of the software sector underscored a growing realization: AI is beginning to impact not just workflows, but revenue models, profit margins, and balance sheets.

Trump Accounts

The newly created Trump Accounts (officially known as 530A accounts) are the latest buzz in family financial planning, though they are currently in a "pre-release" phase. Designed as federally backed, tax-deferred investment accounts for minors, they won't officially launch or accept contributions until after July 4, 2026. The real draw is the pilot program offering a one-time $1,000 government seed deposit for American children born between 2025 and 2028. For eligible families, these accounts are widely considered a no-brainer - it’s essentially "free money" from the government to jumpstart a child's long-term wealth, with the added flexibility of allowing parents and even employers to contribute up to $5,000 annually without any earned income requirements for the kid.

Inflation Surged

Inflation jumped to 3.3% in March, almost a full percentage point increase from February. While "core" inflation (excluding food and energy) remains more modest at 2.6%, the 21% surge in gasoline prices accounted for nearly three-quarters of the monthly jump. This has pushed consumer sentiment to some of its lowest levels in the history of the University of Michigan survey, as families find their purchasing power being clawed away at the pump.

Private Credit

We are watching the ~$2.5 trillion private credit market closely. For several years, private credit has been one of the more popular investment themes (Shiny! New! Sexy!), offering loans made by non-bank lenders, often private equity firms, promising steady and relatively high returns.

However, the structure comes with an important tradeoff: limited liquidity. These investments are not easily bought or sold, meaning investors may not be able to access their capital on demand.

The concern today is that the market has grown rapidly during a period of higher interest rates. If economic growth slows, some borrowers may face increased difficulty servicing their debt. At the same time, investor demand for liquidity appears to be rising. Several large managers - including BlackRock, Morgan Stanley, Blue Owl Capital, and Apollo Global Management - have recently limited redemptions in certain funds.

While this does not necessarily signal a systemic issue, it is a reminder that private credit behaves differently than traditional fixed income, particularly in stressed environments. We have been careful, have not made use of any private credit in our portfolios, and do not expect any direct impact on client portfolios.

Social Security: The 90-Year-Old’s Midlife Crisis

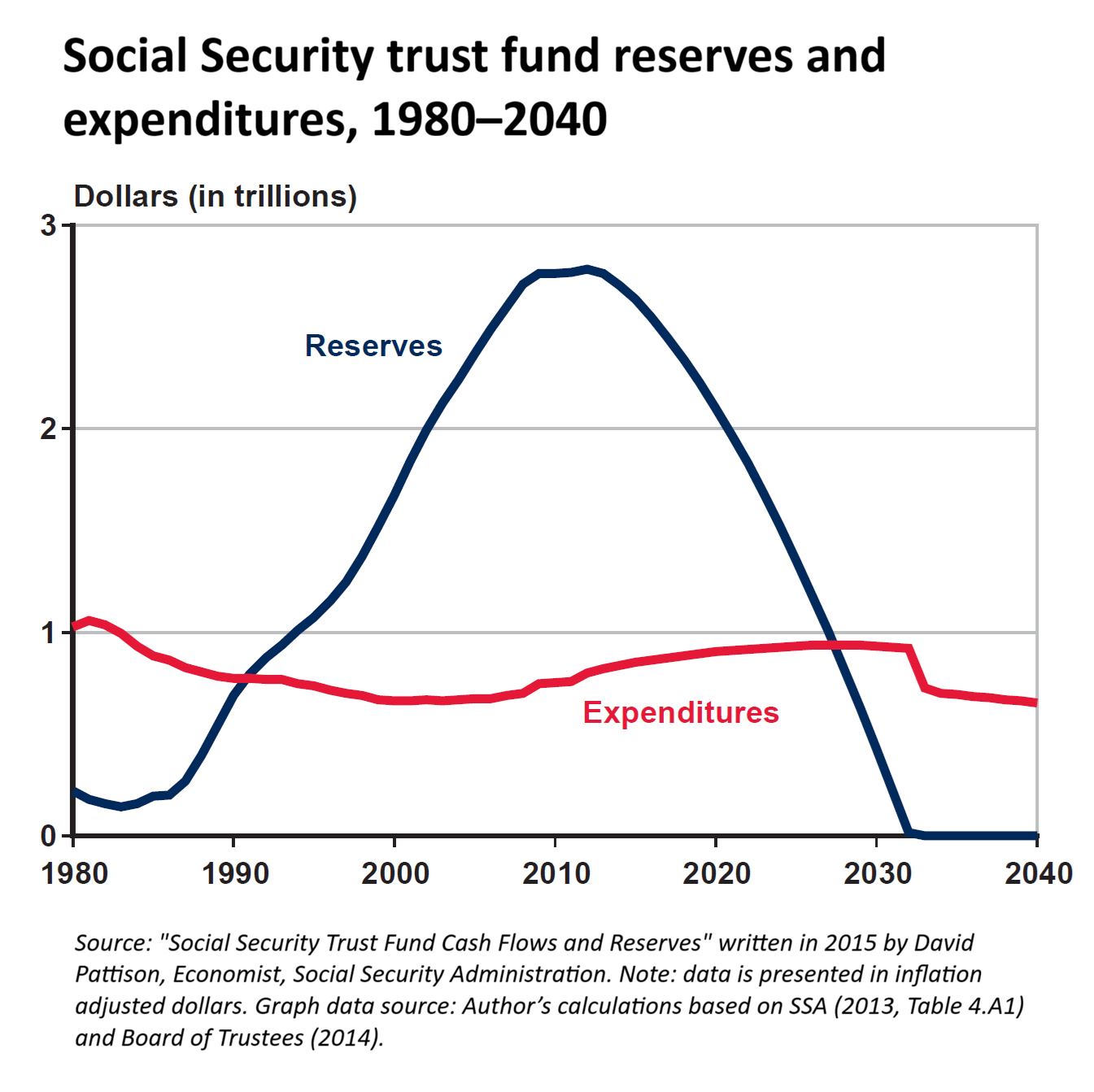

Social Security recently turned 90, but its trust fund is approaching a projected depletion date of 2032. If lawmakers fail to act, beneficiaries could face an automatic reduction of roughly 25% in monthly benefits.

To put that in perspective, Social Security remains the most effective anti-poverty program in U.S. history. According to the Social Security Administration, nearly 22 million Americans rely on it for 100% of their income (wow!). That means millions of Americans could see a meaningful reduction in their primary source of income within the next decade.

The graph below shows the stark reality of reserves relative to expenditures. Hidden in the data is the story of the baby boomers: the reserves increase as Boomers are in their peak earning years, and declined as Boomers reached retirement age. Even though this data is from 2013, little has changed in that macro story, and therefore the graph remains true today.

While there is no shortage of proposed solutions, consensus has been elusive. At its core, the math is straightforward: the Social Security system must either collect more taxes, pay out less in benefits, or adopt some combination of both. The political challenge, of course, is that all of these options are incredibly unpopular.

It’s also worth remembering that the U.S. has faced this situation before. In 1983, Social Security was just months from insolvency. (Note: the reserves vs. expenditures graph has a low point in early 1980’s because of this crisis.) The resulting reforms, negotiated between President Ronald Reagan (Republican) and Speaker of the House Tip O’Neill (Democrat), serve as the modern blueprint for bipartisan compromise. That agreement - which combined gradual increases in the retirement age, the introduction of benefit taxation, and higher payroll taxes – provided for a viable Social Security system for four decades.

The lesson today is similar: meaningful reform is likely to require shared tradeoffs. While the timeline is not immediate, the window to act is narrowing, and the longer policymakers wait, the more difficult those tradeoffs may become. If we use 1983 as a guide, we again might see Congress act in the waning months of 2031 before making any meaningful changes.

Conclusion

We are long-term optimists because the U.S. economy has a relentless habit of adapting to chaos. Remember, volatility is a feature, not a bug. Whether the current volatility is a brief dip or the start of a larger bear market, our strategy remains the same: stay the course and trust the plan.

Reach out anytime if the headlines are getting too loud.

Chris Duke

April 20, 2026

DISCLOSURES

This is being provided for informational purposes only and should not be construed as a recommendation to buy or sell any specific securities. Past performance is no guarantee of future results, and all investing involves risk. Index returns shown are not reflective of actual performance nor reflect fees and expenses applicable to investing. One cannot invest directly in an index. The views expressed are those of Chris Duke and do not necessarily reflect the views of Mutual Advisors, LLC, or any of its affiliates

Investment advisory services are offered through Mutual Advisors, LLC, DBA Context Wealth, an SEC-registered investment adviser.