Two Truths and a Forecast (Please Don’t Tell My Past Self)

All LettersI hope your holiday season was festive and restorative. Our household felt like a non-stop whirlwind between Thanksgiving and New Years!

When I first sat down to write this letter, I worried I might not have much to say. Then I started reflecting on the quarter, and the year as a whole, and realized just how eventful it’s been. From the shock-and-awe pace of the Trump White House, which has issued more executive orders in 2025 than Biden did in four years, to a steady drumbeat of international developments, there’s been no shortage of headlines. Remember the daily DOGE drama? USAID? Liberation Day? The subsequent Trump Tariff Tantrum that sent the S&P 500 tumbling? Add in shifting immigration rules and vaccine policies, and, yeah, it’s been a lot.

A Focus On Q4.

The fourth quarter of 2025 capped an extraordinary year for markets, though the ride was anything but smooth. The longest government shutdown in U.S. history began on October 1 and dragged on for 43 days. And yet, markets proved remarkably resilient.

The S&P 500 gained 2.7% during the quarter and finished the year up 17.9%, including dividends. Along the way, the index set 11 new closing highs in Q4 alone and logged 44 new highs over the course of 2025. That’s particularly impressive when you remember that just months earlier, in April, the market had flirted with a bear market, falling nearly 19% from its February peak.

Monetary policy also played a starring role. The Fed delivered three widely expected 25-basis-point rate cuts during the year, two of them in Q4, bringing the fed funds rate down to 3.5%–3.75% by year-end. (For those at home wondering what this means for you: the highest-yielding bank accounts now sit in that same range, and the average conventional 30-year mortgage has fallen to around 6%.) Still, the December decision came with a notable wrinkle: a 9–3 vote, the most dissents since 2019, signaling a more cautious road ahead as policymakers balance cooling labor markets against stubborn inflation.

After years of trailing U.S. markets, international stocks staged a powerful comeback, with the MSCI All Country World ex-USA Index gaining 32.4% for the year, the widest performance gap versus the U.S. since 1993. The catalyst was a perfect storm: a weakening U.S. dollar (down roughly 9% for the year), more attractive starting valuations overseas, increased European defense spending following Germany’s historic fiscal reforms, and Asia’s expanding role in the AI supply chain.

Emerging markets led the charge. Latin American equities surged 37%, while South Korea’s stock market soared more than 70%. Currency tailwinds played a meaningful role in this outperformance, as a declining dollar boosts international returns for U.S.-based investors. Notably, the dollar just logged its worst year since 2017, pressured by concerns over U.S. fiscal policy, rising trade tensions, and growing diversification away from dollar reserves, often referred to as the “de-dollarization” or “sell America” trade.

Consumer Sentiment

In 2025, consumer sentiment took investors on a roller-coaster ride that ultimately trended lower, ending the year well below where it began. Despite the stock market reaching new highs, the average consumer grew more pessimistic, weighed down by lingering inflation concerns and a cooling labor market. Sentiment started the year on post-election highs above 70 and finished just above 50.

So, what does that actually mean? First, context matters. Consumer sentiment has swung widely over time. During Trump’s first presidency, readings were consistently above 90, before plunging at the tail end of the cycle as the COVID-19 pandemic took hold.

Second, today’s levels are historically rare. Readings in the low-50s have only occurred a handful of times since 1950. To put that in perspective, sentiment never fell this low during the depths of the dot-com bust (77 in March 2003) or even the Great Recession (55.3 in November 2008). The only comparable trough was during the COVID era, when sentiment briefly touched 50 in June 2022.

Third, and most important, consumer sentiment is what economists call “soft data.” In other words, it measures how people feel, not what they’re actually doing. While sentiment was once thought to track recessions reasonably well, peaking before downturns and recovering ahead of recoveries, that relationship began to break down around COVID-19.

Social Security Turns 90

In 2025, Social Security celebrated its 90th birthday. An incredible achievement, but like many 90-year-olds, there are growing concerns about its long-term health. Here’s the good, the bad, and the ugly.

The Good: Social Security is the ultimate poverty fighter. We sometimes forget that it was originally designed as a safety net, not a primary retirement plan. While perceptions have evolved, and many Americans now view it as a core part of their retirement income, it remains the most effective anti-poverty program in U.S. history. Roughly 40% of seniors receive at least half of their income from Social Security, and for nearly 15%, it’s their sole source of income.

The Bad: The math behind Social Security is changing. Life expectancy has increased dramatically over the past 90 years, meaning retirees are collecting benefits for far longer than the system was originally designed to support. At the same time, demographics are working against the program. When Baby Boomers began retiring, the ratio of workers to beneficiaries started to shrink. In 1960, there were about 5.1 workers supporting each Social Security recipient. Today, that number is closer to 2.7 workers per retiree, and it continues to decline.

The Ugly: The Social Security “Trust Fund” is expected to be fully depleted around 2033. In other words, just eight years from now, we’ll be staring down a very real funding gap. There are solutions, but the most impactful ones are also the least popular: benefit cuts of 20%–30%, higher taxes on workers, or significantly increased government borrowing. It’s not hard to see why meaningful reform has been repeatedly kicked down the road.

Things to watch in 2026: Oil, AI, and the Fed

Oil

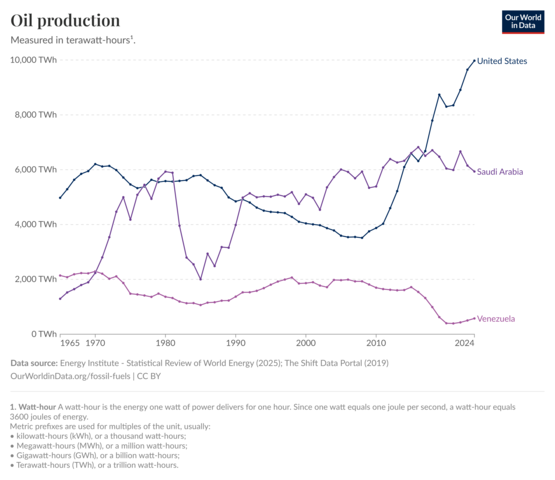

I have found the rhetoric around Venezuela fascinating. While the drama surrounding Venezuelan leader Nicolás Maduro has grabbed headlines, it’s worth noting that this didn’t come out of nowhere, it’s the continuation of a much longer-running narrative. And, as is often the case in geopolitics, lofty language tends to overlap neatly with economic self-interest.

A few oil-related facts help explain why Venezuela keeps popping up in the conversation.

First, Venezuela sits on the largest proven oil reserves in the world, roughly 3.5 times more than the United States, and yes, even more than the Middle Eastern countries you’re probably thinking of. That oil is mostly still in the ground, which brings us to the second point: despite all those reserves, Venezuelan oil production has declined for decades. Meanwhile, global oil consumption has marched steadily higher. The result? Venezuela’s share of the global oil market has quietly shrunk, largely due to years of isolation, underinvestment, and heavy government control of its oil industry.

Third, and this is where things get especially interesting, Venezuela’s oil is the thick, heavy, sour kind (think sludge), while much of the oil produced in places like the Texas Permian Basin is “light and sweet.” Heavy crude is more expensive to refine, which sounds like a downside... except that many U.S. refineries along the Gulf Coast just happen to be specifically designed to process heavy crude. In other words, if Venezuelan production ramps up, the U.S. is in a uniquely good position to benefit. There is a very practical reason America is paying attention, and it may have less to do with drug trafficking than we have been led to believe.

AI spending

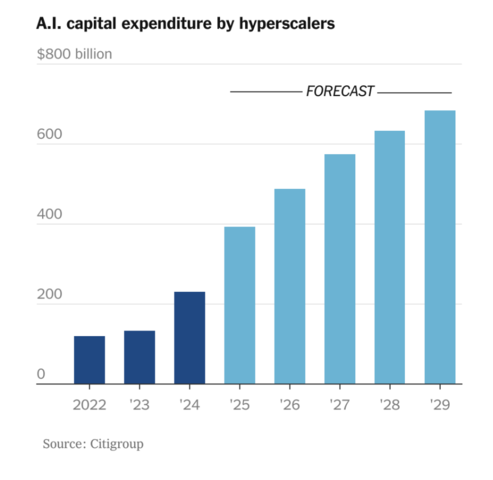

Spending on AI, most visibly through investment in data centers and related infrastructure, has been nothing short of miraculous. A research report from Citigroup estimates that AI-related infrastructure spending could exceed $2.8 trillion through the end of 2029. That’s a dramatic step-change from the pre-AI era, when data-center investment grew steadily but without anything resembling today’s urgency.

So what changed? In short: AI workloads are compute hogs. The servers that power large language models and advanced AI applications require far more processing power, energy, and cooling than traditional cloud or search workloads. If you’re looking for the moment the curve really bent, it was likely November 2022, with the public release of ChatGPT, when AI went from “interesting research project” to “we need more servers, yesterday.”

It’s also worth noting that Citigroup’s estimate applies only to the hyperscalers, the largest players in cloud computing. The so-called Big Three, Amazon, Microsoft, and Google, currently provide well over 60% of global cloud-compute capacity. But they’re not alone. Oracle, Meta, and others are also committing enormous sums to new data-center capacity.

This isn’t just another tech spending cycle, it’s a full-blown infrastructure arms race. And once again, the bill is being paid upfront, with the payoff expected later. Interesting times, indeed.

Outlook for 2026

I’ve spoken with many of you over the years about what I sometimes call two great truths, one rooted firmly in the past, the other staring awkwardly into the future.

The first truth is backward-looking: we’ve just lived through three years of tremendous market growth. According to YCharts, the three-year compounded annual return for the S&P 500 (with dividends reinvested) is roughly 23%. The five- and ten-year numbers aren’t exactly shabby either, both coming in just north of 14%. For context, the long-term average since 1990 is closer to 10%.

Averages, of course, have an annoying habit of eventually returning to their long-term mean. Periods of above-average returns are typically followed by below-average ones. When does that happen? No one knows. Markets have a long history of staying above, or below, that trend line far longer than logic (or patience) would suggest.

The second truth is forward-looking, and it’s this: I hate forecasting. Attempting to make precise predictions in a world as complex as ours is often a recipe for disappointment. Worse yet, we haven’t actually gotten better at it over time. As the saying goes, first coined back in 1965, “The stock market has predicted nine out of the last five recessions.”

I usually describe myself as short-term pessimistic and long-term optimistic. Short-term pessimistic because the daily news cycle can make you depressed, and will eventually drive you insane. Long-term optimistic because history has repeatedly shown that the U.S. economy innovates, adapts, and grows, and that patient investors are rewarded for trusting that process.

And yes, I know I’m contradicting myself, and no, I haven’t lost the plot. But here I stand, stepping cautiously into the forecasting fray: I expect good things from portfolios in 2026.

Here’s the case for a positive market year:

- Inflation continues to trend in the right direction.

- Interest-rate cuts are expected in the first half of 2026.

- The Federal Reserve is projecting continued real GDP growth.

- Analysts expect earnings growth to accelerate next year.

As far as I can tell from the data, we’ve never seen a negative stock-market return in a year when both GDP is growing and interest rates are being cut.

Now, the case against a positive year:

First and foremost, because I just made a prediction, lightning will probably strike me down on my way home from work today, and the exact opposite of my prediction is quite likely to happen! Second, according to Yardeni Research, every single analyst they surveyed is forecasting a positive market return for 2026. Whenever everyone agrees on something, it’s usually wise to be at least a little suspicious.

So where does that leave us?

At the risk of sounding like a broken record, it brings us back to a few core tenets. We don’t chase performance. We invest for the long term and stay the course through short-term volatility, regardless of whether our emotional bias leans optimistic or pessimistic in a given moment. And above all, we believe financial planning is the cornerstone of everything we do. It’s what anchors our investment strategy and provides stability when markets, and headlines, inevitably wobble.

In short, we take the long view. And history suggests that’s still the most reliable strategy of all.

We are ever grateful to serve as your financial advisor, and hope to continue doing so for many years.

Best,

Chris Duke

January 22, 2026

DISCLOSURES

This is being provided for informational purposes only and should not be construed as a recommendation to buy or sell any specific securities. Past performance is no guarantee of future results, and all investing involves risk. Index returns shown are not reflective of actual performance nor reflect fees and expenses applicable to investing. One cannot invest directly in an index. The views expressed are those of Chris Duke and do not necessarily reflect the views of Mutual Advisors, LLC, or any of its affiliates

Investment advisory services are offered through Mutual Advisors, LLC, DBA Context Wealth, an SEC-registered investment adviser.