Debt Slavery or Goldilocks Tax Rates?

All LettersDebt Slavery or Goldilocks Tax Rates?

A Q2 2025 Market Update

The Big Picture: Three Forces Shaping Markets

As we close out the first half of 2025, three major themes continue to drive market sentiment: Tariffs, the Fed, and the BBB (Big Beautiful Bill). Each carries significant implications for your portfolio, and frankly, none of them are fully resolved yet.

Tariffs remain front and center. The correlation between tariff announcements and market swings has been impossible to ignore this quarter. While some deals are evolving, we're still navigating shifting deadlines and ongoing negotiations - the uncertainty isn't over.

The Federal Reserve is under pressure. Trump's public criticism of Fed Chairman Powell has intensified, creating an unusual dynamic. Here's what matters: a recent Supreme Court ruling suggests the president's authority over various boards and agencies doesn't extend to the Federal Reserve. Powell's term runs until May 2026, and historically, Fed chairs can only be removed "for cause"—meaning inefficiency, neglect of duty, or malfeasance. Still, the mere possibility of political interference adds a layer of risk that markets are watching closely.

The Big Beautiful Bill is still being digested. This legislation is so comprehensive that we're still parsing through its long-term implications. What we know: the tax cuts from Trump's first administration, originally set to expire, have been extended.

The Tax Rate Dilemma: Finding the Sweet Spot

Taxes always spark heated debate, but the stakes feel particularly high right now. The fundamental challenge remains: set rates too low and governments can't meet their obligations; set them too high and you stifle economic growth, ultimately reducing tax revenue anyway.

The case for lower taxes centers on the Laffer Curve—a concept popularized during Reagan's presidency in the 1980’s. The theory suggests there's a "Goldilocks" level of taxation that stimulates the economy enough to actually increase total tax revenue by growing the overall economic pie. After all, if tax rates were 0%, there'd be no revenue; if they were 100%, there'd be no incentive to work.

The case against lower taxes is straightforward: we're already running a deficit. The 2024 annual deficit hit $1.83 trillion, adding to our national debt of roughly $36 trillion. We're not collecting enough revenue as it is.

So what does the BBB actually cost us? The non - partisan Congressional Budget Office estimates the bill will add $3.4 trillion to the debt over 10 years—or $4.1 trillion when you factor in additional interest payments. That's roughly 10% added to our existing debt.

The Trump administration disputes these numbers, arguing the CBO hasn't properly accounted for the economic growth that tax cuts generate, nor the revenue from tariffs. If their math is right, the real 10 - year impact would be closer to $1.5 trillion instead of $3.4 trillion.

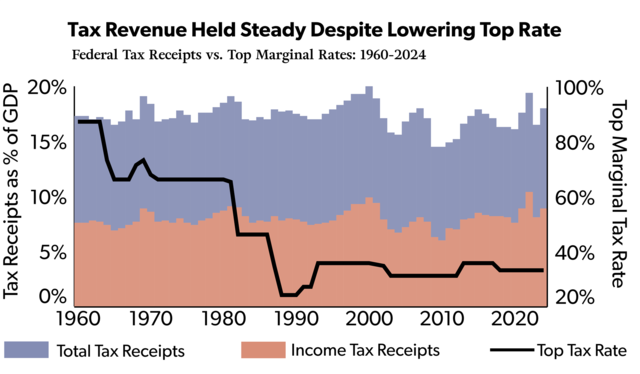

But here's what caught my attention. I recently came across a fascinating chart showing that over the past century, regardless of whether the top marginal tax rate was 35% (today) or 80% (at its peak), tax receipts as a percentage of GDP have remained remarkably steady—between 15% and 20%. It raises an intriguing question: Does the actual tax rate matter as much as we think? (Source: FRED, National Taxpayers Union Foundation)

Elon Musk certainly thinks it does. He reversed his stance from Trump cheerleader and head of DOGE to significant detractor. His take on the BBB? "This immense level of overspending will drive America into debt slavery!"

Quarter in Review

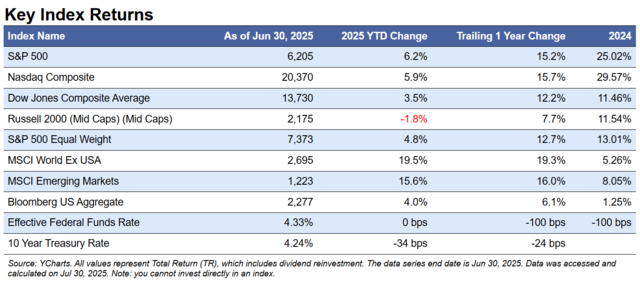

Despite all this uncertainty, the S&P 500 managed to reach a new all - time high by the end of Q2. The journey wasn't smooth—we saw a remarkable 22% swing year - to - date, from - 15.8% on April 8th to +5.5% by June 30th. It's a reminder that markets can climb walls of worry, even when those walls seem particularly high.

Graph of the month

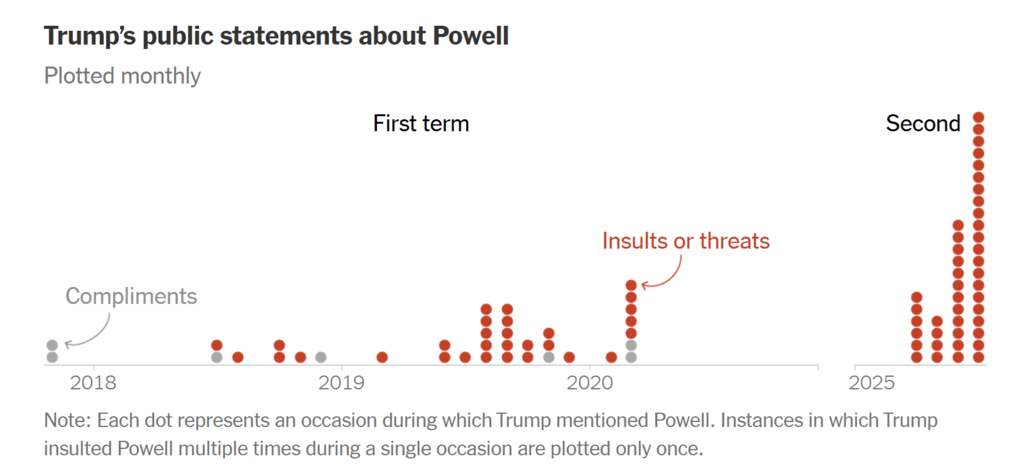

How does Trump feel about Fed Chairman Powell? If read track his public comments, both positive and negative, he is NOT a fan and ramped up the public rhetoric in Q2 2025. Source: NY Times

Looking Ahead

The question isn't whether we'll face continued volatility around tariffs, Fed policy, and fiscal spending—we will. The question is how we position ourselves to weather these storms while staying focused on long - term wealth building.

As always, we'll continue monitoring these developments and their impact on your portfolio. In times like these, maintaining perspective and staying disciplined with our investment approach becomes even more critical.

I trust you have found this review to be informative. If you have any inquiries or wish to discuss any other matters, please don’t hesitate to contact me or any team member.

Thank you for choosing us as your financial advisor. We are honored and humbled by your trust.

Warm regards,

Chris Duke

July 31, 2025

DISCLOSURES

This is being provided for informational purposes only and should not be construed as a recommendation to buy or sell any specific securities. Past performance is no guarantee of future results, and all investing involves risk. Index returns shown are not reflective of actual performance nor reflect fees and expenses applicable to investing. One cannot invest directly in an index. The views expressed are those of Chris Duke and do not necessarily reflect the views of Mutual Advisors, LLC, or any of its affiliates

Investment advisory services are offered through Mutual Advisors, LLC, DBA Context Wealth, an SEC-registered investment adviser.