2023 07 Client Letter - A Lannister Always Pays his Debts

All LettersI hope this finds you well. Those living in the Bay Area enjoyed a relatively cool spring and early summer. But, like much of the rest of the country, July has turned HOT! I hope that you are figuring out ways to keep cool.

A Lannister always pays his debts.

In the fantasy fiction series Game of Thrones, an outsized role is played by the rich and powerful Lannister family. The official family motto is "Here me roar!" which is narcissistic but fitting. There is an unofficial mantra, which is "A Lannister always pays his debts." Throughout the story's arc, various members of the Lannister family use this in different ways: raising armies, propping up economies, and promising retaliation when wronged. In negotiations large and small, this assurance was used to secure better terms.

Meanwhile, closer to home, a fair amount of hand-wringing was going on through the first half of the year as we followed the drama of the "debt ceiling crisis." I consistently believed and communicated to clients that Congress would eventually be pragmatic, end the posturing, and pass a debt ceiling resolution. In late May, Treasury Secretary Janet Yellen warned Congress that June 5, 2023, was the "X Date" when the U.S. would no longer be able to meet all its financial obligations. With only days to spare, Congress passed, and President Biden signed, a suspension of the debt ceiling limit for two years. The full faith and credit of the United States remains tarnished but intact. It is worth noting that the two-year suspension means that the debt ceiling won't be discussed, at least as an existential question, until after the 2024 elections.

I link the Lannisters with the full faith and credit of the United States simply because they are both claims, i.e., things that people believe because there is no evidence to the contrary. In the case of the Lannisters, the claim basically said, "Trust me, I'm good for it." That claim was never questioned or doubted across eight television show seasons. The reason the claim was never questioned was that it had a long track record of being true and had never NOT been true. If there had been a first case where it was not true, the Lannisters would have lost much of their power and sway. The same holds for the United States, which is why I'm thankful that pragmatism eventually won out. Much like the Lannisters, even the most extreme views on both sides of the political spectrum gave a little so that we could proclaim, at least for now, "the U.S. always pays its debts."

Please don't interpret this to mean that I'm not concerned about the U.S. debt level. I am, especially for my children and all future generations. The right time to discuss and disagree about spending money (which is no different than in personal finance) is before you actually spend the money (i.e., during the budget cycle).

Breaking free of the bear

A bear market is defined as a 20% or greater drop in a major market index, usually the broad-based S&P 500 Index. Unlike the better-known Dow index, which comprises only 30 companies, the S&P 500 (which currently consists of 505 stocks) is considered a better benchmark of the overall stock market. From its peak in January 2022 to its most recent bottom in October 2022, the S&P 500 shed 25% of its value. While a 20% peak-to-trough decline defines a bear market, a 20% rise from the most recent low marks the start of a new bull market, at least that is the technical definition. Since the mid-October low, the S&P 500 has advanced 24.4%.

Gaining the upper hand

What's behind the advance? There has been no shortage of anxieties that might trip up investors, including a lot of talk of recession, still-high inflation, rapidly rising interest rates, an ongoing war in Ukraine, an inverted yield curve, and this year's banking crisis. Despite the widespread anticipation of an economic downturn, it has yet to materialize, and employment opportunities continue to expand.

The Federal Reserve is considering raising interest rates further, but the magnitude of these increases has significantly decreased this year.

This year's progress in the stock market can be primarily attributed to the slower pace of rate hikes and the relatively healthy growth of the economy. Furthermore, the fascination with artificial intelligence (A.I.) has significantly boosted the performance of technology stocks.

The Big 7

Technology stocks were the big winners in the first half of 2023. A portfolio that included only The Big 7 – a list which includes Apple, Microsoft, Alphabet (aka Google, including both share classes), Amazon, NVIDIA, Tesla, and Meta (aka Facebook) – and held those stocks in roughly the weights they represent in the SP500, would have risen approximately 68% in the first half o the year. By comparison, the S&P 500 itself rose about 16%. Given that the Big 7 represents about 26% of the S&P 500, removing the Big 7 results in an index or portfolio that was basically flat.

Somewhat counterintuitively, this is a decent demonstration of the value of diversification. The same portfolio of Big 7 stocks was down over 40% from the 2022 high, roughly twice what the S&P 500 was down.

When you look at relative valuations, the numbers are striking. Today the Big Seven portfolio trades with a forward P/E Ratio of 30.4, which makes these stocks more expensive than their long-term average. By comparison, the S&P 500 trades with a forward P/E Ratio of 19, near the long-term average valuation. The midcap indexes trade at a forward P/E Ratio of between 13 and 14, below the long-term average valuation. (A "forward P.E." measures the relative value based on expectations for future earnings.) In plain English, while the Big 7 have performed well year to date, they are expensive relative to their historical average and compared to other investment classes and options.

Inflation and Recession

Recent polls have shown that inflation and recession are the top two concerns of many Americans. There is good news on both fronts. Some economists and pundits have started to refer to the current state of the economy as the "Goldilocks" economy – not too hot, not too cold, just right.

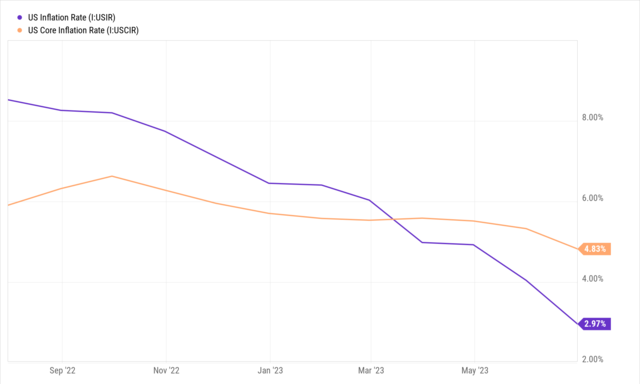

Recently released data shows that year-over-year inflation continues to decline. Inflation has yet to cool to the Fed goal of 2%, which means we may see the Fed continue to increase interest rates this year. If there is a flattening of the monthly inflation reporting (or an increase), you can undoubtedly count on the Fed to start raising rates again. The ideal situation is a "soft landing," where the Fed can reach maximum employment, achieve 2% inflation, and not overcorrect and cause a recession.

Figure 1: Headline Inflation (with food and energy) and Core Inflation (excluding food and energy). July 2022 to June 2023. Source: YCharts

The likelihood of a recession is decreasing, although additional rate increases by the Fed could tip the scales. Historically speaking, most recessions are not widely discussed and predicted in advance. In reverse order, the recessions of the last thirty years include Covid (2020), Great Housing Crisis/Great Recession (2008-2009), and Dot Com (2001). Only a few people predicted these events in advance; even then, they were widely discounted. By contrast, CEOs, politicians, talking heads on T.V., and baristas have widely predicted and discussed the potential for a recession.

I have a highly unscientific working theory that I sometimes lean on. I don't have anything against baristas (and I certainly love the product they peddle), but I do have something I call the "barista rule." The rule states that if a barista asks about a financial-related topic, I know it's overblown. These are actual cases in point: buying rental property with no down payment (circa 2007), investing in gold (circa 2012, and also ongoing), and Cryptocurrency (yesterday). Since I was recently engaged in a conversation about the likelihood of a recession by a barista, the rule implies that we are not headed for a recession.

Do not worry. There is also empirical data to support the case for no impending recession. Of the 14 empirical indicators I follow, 11 are positive (jobs data, GDP data, oil, inflation, etc.), and 3 are negative (LEI, inverted yield curve, manufacturing PMI). This is a significant improvement from three months ago when we had six negative readings.

Wrap Up

We don't believe market timing is a realistic strategy. Just as no one rings a bell at a market peak, no one rings a bell when a bear market ends. Market timers sometimes get lucky, but one must consistently catch the timing and direction correct – twice – to come out ahead. The likelihood of that happening over extended periods is very close to zero.

Just as 2022's bear market surprised most, many timers failed to anticipate the turnaround this year against the backdrop of a hefty dose of negative sentiment when the year began.

Successful long-term investors steer clear of chasing after trendy fads and the temptation to time the market. Instead, they adhere to a well-established and disciplined strategy that has consistently proven to be the most profitable path.

It's always a privilege and a humbling experience to be chosen as your financial advisor. Thank you for your trust and confidence in our services.

DISCLOSURES

This is being provided for informational purposes only and should not be construed as a recommendation to buy or sell any specific securities. Past performance is no guarantee of future results, and all investing involves risk. Index returns shown are not reflective of actual performance nor reflect fees and expenses applicable to investing. One cannot invest directly in an index. The views expressed are those of Chris Duke and do not necessarily reflect the views of Mutual Advisors, LLC, or any of its affiliates

Investment advisory services are offered through Mutual Advisors, LLC, DBA Context Wealth, an SEC-registered investment adviser.